The projections for the next 12 months suggest that business leaders need to strap themselves in for a bumpy ride. Some continue to enjoy AI highs. Others are figuring ways to capitalise on the new pathways for international trade. An increasing number of observers are concerned about market bubbles, unemployment, low or negative growth projections and the quickening pace of geopolitical risk.

It’s a picture that seems to shift and change depending on sector and geography, but there are certainly some themes to emerge. Criticaleye spoke to Members of its global Community for their views on the key trends and watchpoints for leaders in 2026.

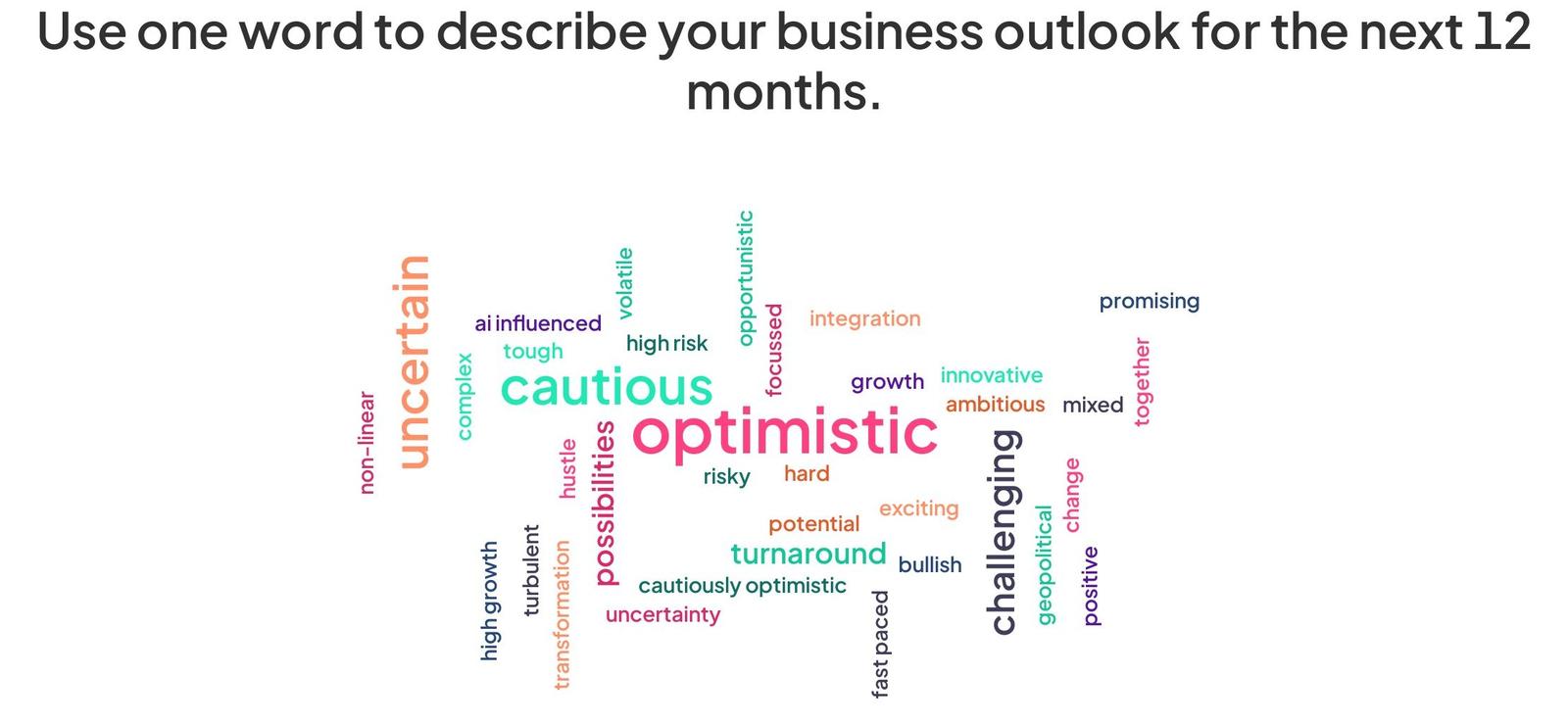

This is what they said:

In ASEAN, domestic consumption has been relatively steady. Central banks have been cutting rates. A lot of Asian governments are doing some form of fiscal stimulus. … All this is trying to keep the whole economy growing. So this year [2025] is going to be better than expected. Then the question comes to ‘what happens in 2026?’ because the growth base in 2025 is much higher, and growth numbers are completed year-on-year. So, if you have a higher base, you're going to have more headwind going into 2026.

At present, it looks like a very modest slowdown in the region. In fact, it’s a very benign scenario. There's no real crisis you can eyeball. This is predicated on two things: one is that markets have started to realise that tariffs can be negotiated. A lot of assumptions are that companies will go direct to the US administration and negotiate the tariffs, so it's not going to be as punitive.

The second is that if you look at US-China tensions today, it has reached a bit of an even keel, in the sense that there is some form of truce. Some may say it's just kicking the can down the road, because the problems haven't gone away, but at least we have some form of agreement and that keeps things in check for now. And we do expect the Fed to continue cutting rates.

The last point is, we don't know what we don’t know. We are very good at seeing what's in front of us, which is geopolitical risk, tariffs and idiosyncratic risk in individual countries. But if you think back to what has happened in the last 15 years, typically it’s the curve ball that gets you. Nobody expected a health pandemic. Nobody expected that the subprime crisis in the US would cause a global financial crisis. Typically, it's not the risk that's in front of you that will get you into the next crisis.

Response taken at Criticaleye's Asia Leadership Retreat, November 2025

Mike Bell, Interim Macro Strategist, Elston Consulting:

The UK labour market is deteriorating with employment in cyclical sectors declining. Hospitality and retail jobs have been badly affected because of after-tax labour costs for minimum wage workers rising faster than pre-wage profits. Business surveys point to a continued decline in employment. Recession risk is therefore elevated.

UK inflation, meanwhile, is mainly being driven by food prices in only a small number of categories, mostly related to cattle. [Excluding] food, shop price inflation is weak, as businesses are struggling to pass on higher labour costs to struggling consumers. Inflation is likely to fall quite sharply and hence UK rates are likely to fall by more than the market expects.

In Europe, strong job growth in Spain is masking weaker job growth elsewhere. In Germany, cyclical employment is falling as companies struggle with high energy prices, tariffs and competition from China. There is also hardly any cyclical job growth in France. Stripping out energy, oil and food there is very little domestically driven inflationary pressure on the continent.

In the US, near-term recession risk is lowest of the major developed market economies because of strong AI-driven CapEx and some moderate stimulus from the OBBBA [One Big Beautiful Bill Act]. However, cyclical job growth is also very close to stall speed and there is a risk that a squeeze on smaller company margins from tariffs and squeezed lower income consumers could lead the current decline in hiring to turn into outright firing of workers. Recession risk for 2026 is therefore likely still higher than markets are pricing, despite being lower than in the UK and Europe. US equity valuations are also stretched.

China continues to face significant problems in its property market, and the poor demographic outlook means that Chinese property prices are under structural rather than just cyclical pressure. The same can be said for Japan and Europe, where the population is also set to decline.

Mary Jo Jacobi, Member of Advisory Board, Rothermere American Institute, University of Oxford and Board Mentor, Criticaleye:

The US outlook is good, but mixed due to some ‘known unknowns’. The huge tax refunds to individuals that will land in the first quarter should have a stimulus effect, but markets will be concerned about the transition at the Fed when Jerome Powell retires in late Spring. Thereafter, we’ll have the uncertainty surrounding the Congressional mid-term elections when the party in power in the White House usually loses seats. This could signal the undoing of much of the President’s economic agenda if the Democrats take power in January 2027. Overall, I expect growth to be modest.

The tariffs have brought in a lot of revenue to the US Treasury and hundreds of millions of dollars in inward investment to the US, which should be a stimulus for growth and jobs. I believe in free but fair trade; the tariffs have brought some balance to a number of US trading relationships. However, the litigation surrounding them has added to an already uncertain environment for both businesses and consumers.

I’ve lived through many [US Government] shutdowns, including several when I worked for President Reagan. In the immediate term, they’re moderately disruptive. In the long term, they’re a political talking point. There could be a further shutdown early next year [2026] when the Continuing (Budget) Resolution expires, which will contribute to the uncertainty surrounding the November mid-term elections.

It sure looks like we’re in an AI bubble right now, with the investment, the acquisitions and the growth of data centres to sustain the industry. … AI is the future, one way or another, and I think we can look to the tech companies to keep hope alive as long as possible, so I see a correction rather than the bubble bursting completely.

I’m hoping for and dreaming of a very happy new year with peace dividends for the world and reduced tariffs and lower taxes in the US.

The global economic outlook very much depends on the US, and whether the US economically is in a strong place because of the tariffs, or a weak place, because the implications for those two things are very different. If the US has a tighter economic position, it's going to be a really difficult year. If the US has a better position, it will be a much more positive perspective.

The constant drive towards technology is not going to dissipate. … Are the capital valuations of some of those technology businesses going to slow down? They might, because certain areas are so frothy. … This could actually be quite good because capital might flow and disperse in a more differential way. As such, sectors that have been undervalued possibly have an opportunity to rebalance.

However, you've still got significant questions about the consumer around the world, and the implications of consumer spend being more constrained … I think you've got natural elements of more growth in certain places, but you've still got all the same geopolitical issues, social issues, employment, cost of living.

This means there will be more pressure on leaders, … whether that's activist shareholders, Boards, customers – you’ve got to be pretty resilient and be able to retain a high level of performance. But within that, there’s huge opportunity, because actually leadership differential is easier in a tight marketplace where that pressure is flying around … I think you'll see a continual drive for performance, but it's not going to be a nice place to be a leader because the backdrop is a negative environment. There is constant media negativity and a geopolitical landscape that isn't easy to read and can change very fast, and that's the same locally, nationally and on a global basis.

Tom Attenborough, Head of International Business Development - Primary Markets, London Stock Exchange Group:

London's attraction to international companies as a place to raise capital and as a place to diversify the investor base remains as strong as ever. We've seen 22 IPOs and £2.1 billion raised [in 2025], and a further eight companies have added a London listing in 2025. Together they represent a combined market cap of over £56 billion. Over three quarters of that [£2.1 billion of] capital has been raised in Q4 2025, including some reasonably significant transactions from UK companies like Shawbrook and Princes Group. The biggest IPO of the year has come from US power and data centre business – Fermi – dual listing in London and raising £584 million.

In addition, we have seen listings of The Magnum Ice Cream Company and The Generation Essentials Group in December, underscoring the international appeal of the London Stock Exchange.

With the momentum we have seen across UK capital markets this year, we are optimistic going into 2026. We’ve seen the small-cap activity start to tick up in the second half of 2025. The mid-cap activity in the latter part of the year has really started to go through the gears. The UK’s ambitious reform agenda also continues, with focus on ensuring that private and public companies can access the vital capital they need at every stage of their development. In addition to a growing pipeline of potential listings in 2026, we are looking forward to seeing the first auctions on our new Private Securities Market, providing liquidity to shareholders of private companies.